My sibling is the administrator and also living in your house on the property. However, he bought another Visit this page 40,000 bucks in remodellings which he need to have know can not have been paid. Now he wishes to obtain a CHIP funding for his portion of the estate and also wants us various other 3 recipients give him title to the estate so he can pay for these debts.

- Originally, if these repayments are not made, the loan provider would reserve several of the undrawn financing earnings into an escrow account to pay those costs.

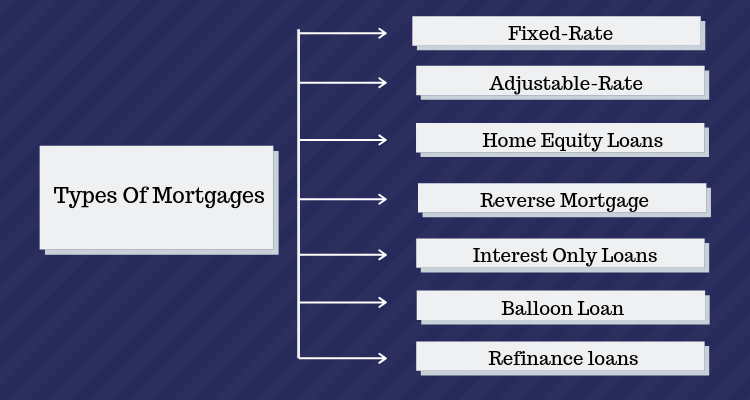

- Single-family dwellings and multi-family systems approximately fourplexes are qualified for a reverse mortgage.

- A reverse home mortgage is a doubtful proposal if you have sufficient earnings to Click to find out more pay your bills or agree to offer your home to use the equity.

- Lots of others wound up losing cash with a reverse mortgage.

A reverse mortgage is not for everybody, but it's not something to be embarrassed of either. As a matter of fact, several wise middle-class and also wealthy homeowners use a reverse mortgage purposefully-- for example, as a safety net in case of emergency situations, or as a monetary device to increase one's liquidity. Today, financial consultants are significantly seeing them as an essential choice and useful monetary devices to be taken into consideration.

Real Estate Tax As Well As Property Owners Insurance Policy To Pay

If the answers to those inquiries are questionable, you need to think about a safer financial path like a typical residence equity loan or credit line. Considering that 2009, reverse-mortgage losses have cost the Federal Housing Management get fund $12 billion. That coincides fund that insures low-income beginners to the real estate market. The good news is you or your estate will never ever need to pay a loan provider more than the marketplace worth of your house. The bad news is Uncle Sam got tired of paying the difference. If you stay in a reverse-mortgage residence in Buffalo and also make a decision to retire to Florida, you'll have to offer the residential or commercial property.

Reverse Home Loans May Be Useful In Retirement If You Mind The Challenges

That compares to less than 3% of federally-insured typical mortgage that are seriously delinquent. It said they told borrowers they would not need to make monthly repayments or face repossession, and really did not inform them about the dangers of stopping working to pay property taxes. You are obliged to spend for real estate tax as well as insurance coverage along with maintenance.

Obtaining A Reverse Home Mortgage Is Almost Never Ever An Excellent Suggestion

The home loan likewise comes due if the property owner moves or sells the home, fails to pay taxes and insurance coverage or does not make needed repairs. Numerous large financial institutions have stopped creating reverse home loans, though they are still offered at smaller financial institutions and also credit unions. The CFPB record said the by the time the average homeowner turns 69, a reverse mortgage expenses $2,300 more http://johnnyipdv042.lucialpiazzale.com/just-how-does-a-reverse-mortgage-job than the gain in Social Security advantages.

Similar to any kind of economic item, you ought to seek advise from your relied on consultant and careful consideration and also viability should be reviewed. The truth is reverse mortgages are exorbitantly costly car loans. Like a normal home mortgage, you'll pay different costs and also shutting costs that will complete hundreds of dollars. For instance, making use of the calculator on the National Opposite Mortgage Lenders Association site, the total charges and also prices on a flexible price $200,000 reverse mortgage would certainly have to do with $10,400. The charges include a lending institution origination cost, an in advance home loan insurance policy charge, and common closing prices such as assessment, declaring, title search and also title insurance policy costs. In comparison, on the Bankrate 2013 Closing Prices study, the nationwide standard was $2,402 to shut on a $200,000 very first mortgage.